A report released Thursday by Adobe Digital Index provides Reason #4,327 why it never made any sense for Apple to build an integrated TV set: Apple devices already dominate over-the-top and TV Everywhere viewing, which is what “TV” is going to be the future.

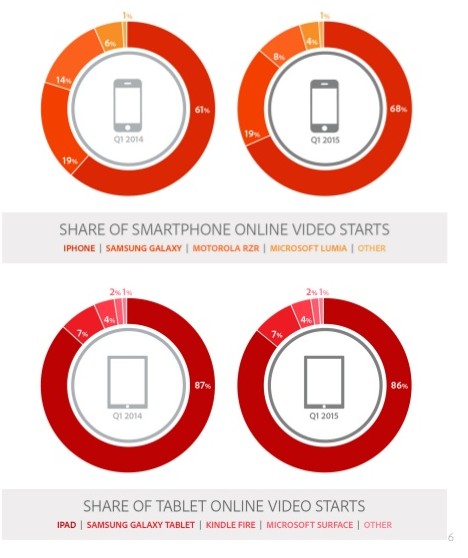

According to the report, nearly one in four (24 percent) of all unauthenticated online video starts, including desktop, set-top and mobile, happen on an Apple mobile device. And as mobile viewing in general increases as a share of total online video viewing, Apple’s share is poised to increase disproportionately. According to the report, Apple devices (iPhone and iPad) account for more than two-thirds of all mobile views.

Apple devices also now dominate in authenticated (TV Everywhere) online viewing. In the first quarter of 2015, iOS devices accounted for 47 percent of online authentications, up from 43 percent a year ago, more than tripling the share of authentications via Android devices or via browsers. Again, as TV Everywhere usage increases overall — now up to 13.2 percent of pay-TV subscribers — Apple will benefit disproportionately due to its dominant market share in authenticated viewing.

{kind=link}

As I noted in a previous post, mobile is the critical pathway to the living room for both Apple and Google. And Adobe’s data clearly suggest that Apple’s OS dominance in mobile video is beginning to translate into a significant beachhead in the living room.

The Apple TV set-top box’s share of authenticated views doubled year-over-year in the first quarter, to 10 percent, helping to drive a 4X increase in the share of total authentications happening on the set-top.

Like the mountain coming to Muhammad, the TV mountain is coming to Apple. Why build its own mountain?

Like the mountain coming to Muhammad, the TV mountain is coming to Apple. Why build its own mountain?

Another question raised but not answered by the Adobe data, however, is why Apple apparently feels the need to create its own, virtual pay-TV service. It already dominates only pay-TV viewing without spending a dime on content costs. What more would Apple get by offering its own service?

One thing it would get, of course, is subscription fees. But for a company with revenue of $212 billion last year and a market cap approaching $1 trillion, it will take a lot of subscription fees to move the needle very far. And, as any traditional pay-TV provider can tell them, content costs take a big and ever-growing bite out of pay-TV subscription fees.

It would also, presumably, gain the ability to insert ads directly into the streams, just as traditional cable operators do. But Apple has long been ambivalent about the advertising business.

A virtual pay-TV service would also align Apple’s video strategy with its music strategy, by moving it away from a transactional, download-based business model to one based on subscriptions and access. I suspect its primary motive at this point is simply the opportunity to build a fully Apple-fied user experience around TV from the ground up and to draw TV viewing deeper into the iTunes/iOS ecosystem.

But if I had to guess, I’d guess that launching its own pay-TV service is a fallback position for Apple. As I discussed in a blog post last summer for GigaOM Research (moment of silence) I think its preferred approach — the one it was clearly working toward until recently — was to create a kind of universal, mobile-centric TV Everywhere experience that could be integrated with and overlaid onto a user’s existing pay-TV service. Apple would control the UI and UX, which would be consistent across devices and would leverage all of the capabilities of Apple devices, but the operators would retain control of their customer relationships. Monetization for Apple would be via advertising, or more likley, via rev-share or bounty with the operators for helping reduce cord-cutting and churn.

Such an approach would have been consistent with Apple’s historical pattern of leveraging its user’s existing investment in content and services to create new, Apple-fied products and services. When first introduced, iTunes was an application for managing your CD collection. It was only after iTunes had taken over everyone’s hard drive music collection and was being used to move music from PC to iPod that Apple launch the iTunes Music Store for downloaded music.

With the iPhone. Apple leveraged consumers’ existing investment in basic mobile voice and text service to introduce new type of mobile user experience while sharing the customer relationship with the wireless carriers. Over time, the iPhone App Store became a platform for launching entirely new types of services. A similar dynamic might well have emerged from a universal TV Everywhere application, which could have become a platform for launching new video services independent of the traditional service providers.

As the Adobe data make clear, the device components of such a strategy already in place and proceeding according to plan.

What changed, I suspect, is that the pay-TV operators grew wary of sharing with Apple, and decided their best course was to control their own TV Everywhere destiny. In the meantime, cord-cutting has accelerated and the networks have grown more open to making their linear feeds available to over-the-top service providers and more flexible about bundling, creating an avenue for Apple to go it alone.

But that’s a riskier and more expensive strategy than surfing on someone else’s investment, which I still think Apple would have preferred.